As the 2025 G7 Finance Ministers and Central Bank Governors’ meeting unfolds in Banff, Alberta, Canada finds itself at the center of discussions on global economic stability. Amidst rising trade tensions and domestic economic challenges, Canada’s position within the G7 is both pivotal and precarious.

1. Fiscal Health

- Net Debt-to-GDP Ratio: Canada maintains the lowest net debt-to-GDP ratio among G7 nations, projected at 41.6% in 2025. This favorable position is attributed to substantial financial assets, including the Canada Pension Plan and Employment Insurance reserves.

- Gross Debt-to-GDP Ratio: Despite the low net debt, Canada’s gross general government debt is estimated at 112.5% of GDP, reflecting the total liabilities without accounting for financial assets.

2. Economic Growth

- Real GDP Growth: The Bank of Canada has revised its 2025 growth forecast to 1.8%, down from an earlier estimate of 2.1%, citing trade tensions and policy measures affecting population growth.

- Per Capita GDP: While overall GDP has shown resilience, real GDP per capita growth has been modest, averaging around 0.3% annually over the past decade.

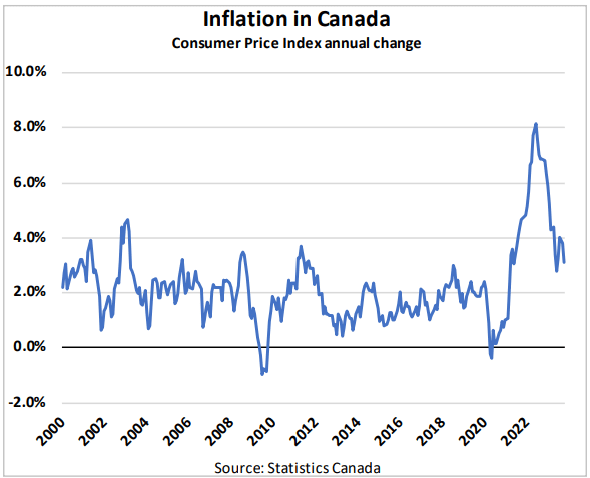

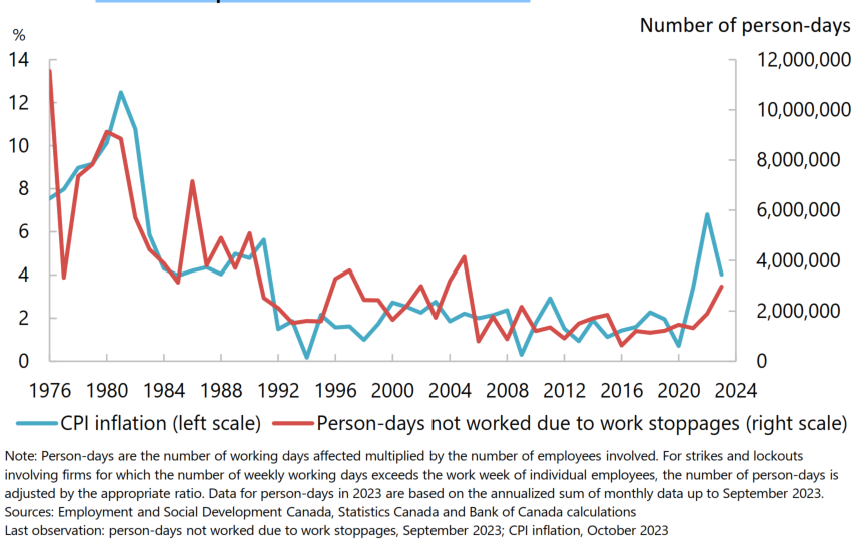

3. Inflation and Monetary Policy

- Inflation Rate: Headline inflation decreased to 1.7% in April 2025, primarily due to falling energy prices and the removal of the federal carbon tax.

- Core Inflation: Core inflation measures, which exclude volatile items, have risen above 3%, indicating persistent underlying price pressures.

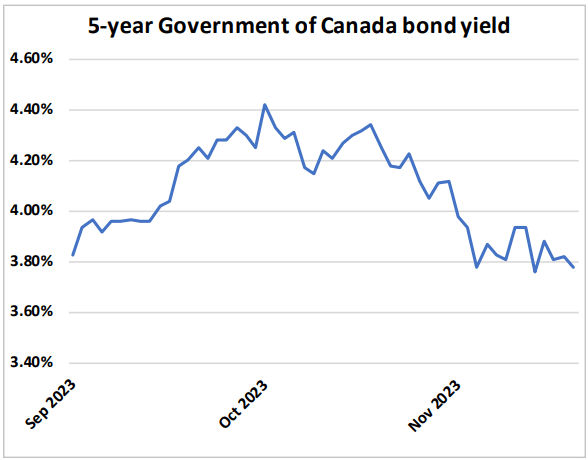

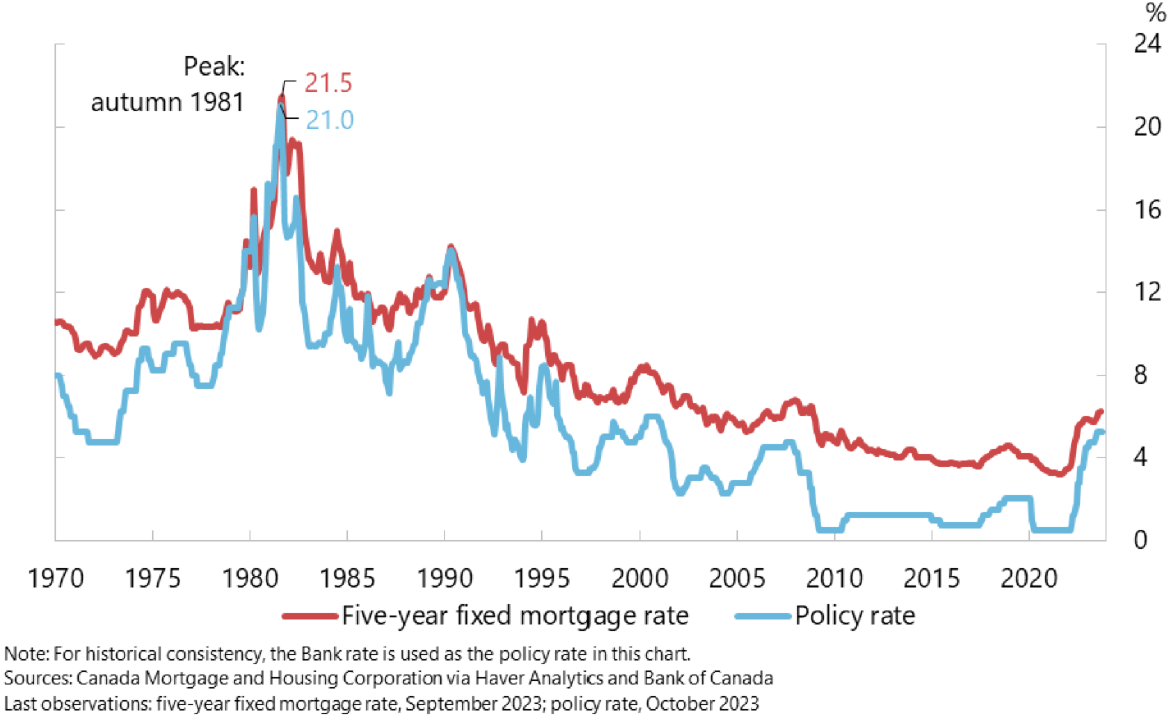

- Interest Rates: In response to economic conditions, the Bank of Canada reduced its key interest rate to 2.75% in April 2025, marking a series of cuts totaling 2.25 percentage points over several months.

4. Labour Market

- Unemployment Rate: As of April 2025, Canada’s unemployment rate increased to 6.9%, the highest since November 2023, with over 1.6 million people unemployed.

- Employment Trends: Employment remained largely unchanged in April, with a net gain of 7,400 jobs. However, employment among core-aged women (25 to 54 years old) declined by 60,000, while increases were observed among older workers and core-aged men.

5. Productivity and Structural Concerns

- Labour Productivity: Canadian labour productivity improved by 0.47% year-over-year in December 2024, following a period of stagnation. Despite this uptick, productivity growth remains below historical averages, raising concerns about long-term economic competitiveness.

- Structural Challenges: Canada’s economy faces structural issues, including low investment in machinery and equipment and a reliance on consumption and real estate sectors. These factors contribute to the country’s lagging productivity compared to other advanced economies.

Conclusion

Canada’s fiscal prudence, evidenced by its low net debt-to-GDP ratio, positions it favorably within the G7. However, challenges such as modest economic growth, rising unemployment, and persistent productivity issues underscore the need for strategic policy interventions. Addressing these structural concerns is crucial to ensuring sustainable growth and maintaining Canada’s economic standing among its G7 peers.